By Stephen Putnins, Partner and Amiinah Dulull, Lawyer

Fast Facts

Your next steps

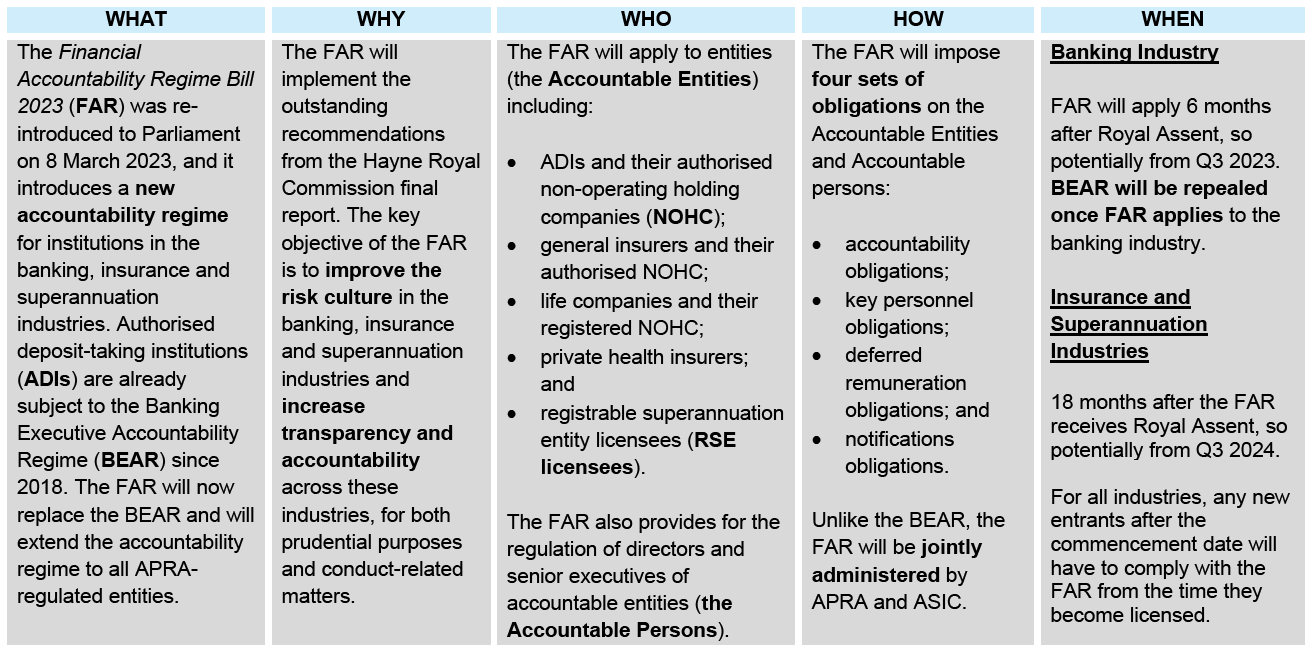

For the banking industry, the earliest potential commencement date of the FAR is the third quarter of 2023 and for the insurance and superannuation industries, the earliest is the third quarter of 2024. With significant obligations on institutions in the banking, insurance and superannuation sectors and their directors and senior executives, alongside heavy penalties and onerous breach reporting requirements for non-compliance, it is time to prepare for the commencement of the FAR.

This new regime will cause Accountable Entities to considerably enhance their core risk and governance arrangements and potentially restructure management to reflect Accountable Person positions and responsibilities. For the entities not already subject to the BEAR, this new regime will necessitate the allocation of additional resources and processes in governance, risk and compliance because substantial work will need to be undertaken to ensure compliance when the FAR commences. The potential fines are very large and will be a significant additional source of risk, especially for RSE licensees and their directors who will be unable to recover civil penalties from a fund. Many ADIs now would have well-established accountability frameworks due to the BEAR, but they will nevertheless need to be revisited and reviewed to ensure compliance with the FAR.

For all entities subject to the FAR, significant work will need to be undertaken to (non-exhaustive):

- identify and map Accountable Persons;

- identify significant related entities;

- train Accountable Persons on their new responsibilities and liabilities;

- prepare the accountability maps and statements (for some entities only); and

- reassess coverage under their insurance policies, contracts, deeds of access and indemnity.

We have put together the following (non-exhaustive) list of considerations for entities subject to the FAR, as they begin preparing for it by implementing or updating their accountability frameworks:

Management Structures

- The FAR will significantly extend the regulators’ powers in relation to an Accountable Entity’s internal management. Accountable Persons will face the prospect of disqualification (as under the BEAR).

- The regulators and Minister have considerable discretions and could heavily shape and dictate management structures of Accountable Entities by determining Accountable Person positions and their responsibilities.

- Entities should consider reviewing accountability principles, delegation of authority frameworks, and board and management committee frameworks in light of the FAR.

Accountable Persons

- Entities should consider identifying Accountable Persons within their organisation and assist them in understanding their responsibilities. This may be in the form of training, development of frameworks and other guidance documentation and by embedding the FAR within the firm’s culture.

Monitoring, oversight and reporting

- Accountable Entities should consider establishing routine assurance monitoring programs to ensure ongoing compliance with the FAR requirements. This would facilitate the proactive and early detection and avoidance of FAR-related breaches and assist in the development and maintenance of robust FAR-related controls.

- Results of ongoing monitoring and oversight can be presented to the Accountable Entity’s board and senior management for reporting purposes.

Type of support we can provide

Our team has significant experience advising ADIs on the full implementation of the BEAR including preparing accountability statements and mapping and establishing a ‘reasonable steps’ framework. We also have significant experience at the back end when things go wrong, and accountabilities are called upon by a regulator. We have experience liaising with APRA, ASIC and AUSTRAC with respect to BEAR related matters.

Pre-commencement support

Given our prior experience with the BEAR, we are well placed to provide entities with in-depth support and insights throughout their implementation of the FAR.

We can provide entities support with drafting and reviewing FAR-related documentation and templates; facilitating workshops to support the implementation of the FAR; and providing detailed advice and feedback on the steps taken by entities to implement the FAR.

Post-commencement support

After the FAR comes into operation, we are able to provide continuous assistance with post-implementation review focused on particular aspects of the regime, for e.g. clarity on accountability obligations, adequacy of reasonable steps taken; and other ad hoc assistance and advice. We can also represent you and/or your directors and executives when things go wrong and Accountable Persons are directly impacted, including liaising with the regulators.

Detailed overview of the FAR

What is the FAR and why is it being implemented?

It is an extension of the BEAR

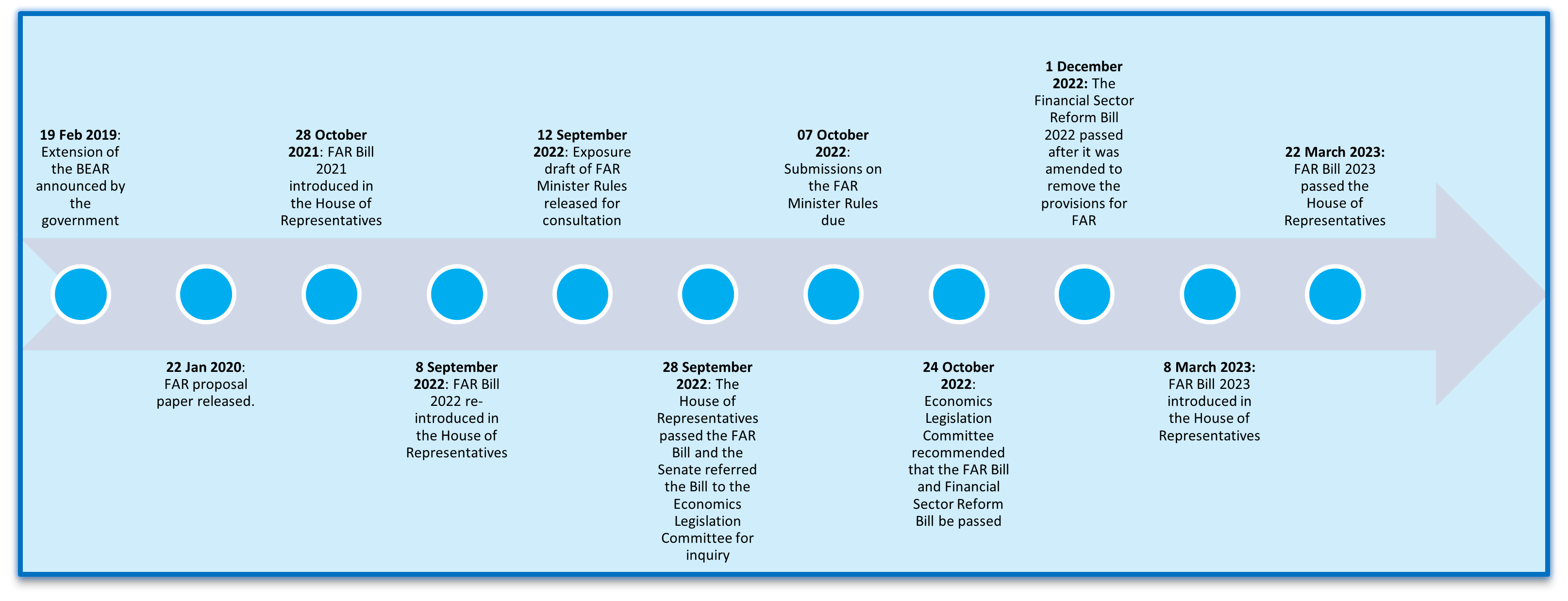

The BEAR became law in 2018 and it was introduced to improve the risk culture of ADIs and to increase transparency and accountability in the banking industry. New accountability obligations were set out in the Banking Act 1959 and this regime is being administered by APRA. The Hayne Royal Commission Final Report (Hayne’s Final Report) recommended the implementation of recommendations that would extend the BEAR to all APRA-regulated entities.

As part of the Government’s response to Hayne’s Final Report on 4 February 2019, the Government announced it would implement:

- recommendation 3.9—to extend provisions modelled on the BEAR to RSE licensees;

- recommendation 4.12—to extend provisions modelled on the BEAR to insurers regulated by APRA;

- recommendation 6.6—to have APRA and ASIC jointly administer the BEAR;

- recommendation 6.7—to make it clear that ADIs and their accountable persons must deal with both APRA and ASIC in an open, constructive and cooperative way; and

- recommendation 6.8—to have APRA and ASIC jointly administer the proposed new regime.

The Financial Accountability Regime Bill 2023 (FAR Bill 2023) introduces a new accountability regime for the banking, insurance and superannuation industries. The FAR Bill 2023 contains the same design specifications proposed by the previous Financial Accountability Regime Bill 2021 (FAR Bill 2021) introduced by the former government in October 2021, which lapsed when Parliament was dissolved.

The stated objective of the FAR is to:

- establish clear standards of conduct by imposing a strengthened responsibility and accountability framework for directors and senior executives across all APRA regulated industries;

- increase transparency and accountability of financial entities; and

- improve risk culture and governance for both prudential and conduct purposes.

On 8 September 2022, the FAR Bill 2022 was introduced with the Financial Sector Reform Bill 2022. Collectively, the bills establish the FAR regime to impose accountability, key personnel, deferred remuneration and notification obligations on directors and senior executives of financial entities in the banking, insurance and superannuation industries. On 28 September 2022, the House of Representatives passed the Financial Accountability Regime Bill 2022 and associated bills. However, on 1 December 2022, the Financial Sector Reform Bill 2022 passed after the FAR provisions were removed. A public hearing of the Economics Legislation Committee (Committee) was held on 14 October 2022. On 24 October 2022, the Committee recommended that the bills be passed. The Committee stated that the package of the bills will ensure a well-functioning framework for resolving disputes within the financial system to safeguard consumer trust and confidence. However, on 1 December 2022, the Financial Sector Reform Bill 2022 passed after the FAR provisions were removed.

On 8 March 2023, the FAR Bill 2023 was introduced in the House of Representatives. The latest FAR Bill 2023 is almost identical to the 2022 version – the only substantive change is to section 16, which amends the Minister’s power to grant exemptions to Accountable Entities. The FAR Bill 2023 clarifies the scope of the Minister’s power and provides for parliamentary oversight by requiring that any exemption is made by way of notifiable instrument including a statement of reasons. On 22 March 2023, the FAR Bill 2023 and the Financial Accountability Regime (Consequential Amendments) Bill 2023 passed the House of Representatives.

The FAR will apply to the banking industry six months after Royal Assent and to the insurance and superannuation industries 18 months after Royal Assent.

Timeline – the FAR so far

The timeline below provides a snapshot of the FAR’s journey so far and what is coming up next.

Scope of the FAR: Who will have to comply with the FAR?

Accountable Entities

The FAR will apply to ADIs; general, life and private health insurers; RSE licensees; and NOHCs of ADIs and insurers. These entities will be the primary entities regulated under the FAR and referred to as Accountable Entities under this new regime. These entities are further distinguished between core notification or enhanced notification entities (this distinction is mainly for the purpose of the notification obligations which we cover at the end of this article).

Significant related entities

Banking and insurance industries

Accountable Entities also have some obligations in relation to their significant related entities (SREs) (which can include entities incorporated and operating outside of Australia). An entity will be an SRE if it is a subsidiary of an Accountable Entity and its effect on the latter is material and substantial. For the banking and insurance industries only, an SRE can only be related to one Accountable Entity – i.e. its closest parent entity.

Superannuation industry

In contrast to entities in the banking and insurance industries, an SRE of an RSE licensee can be a wider variety of entities in the superannuation industry.

SREs of RSE licensees with a ‘material and substantial’ effect on the latter can be:

- subsidiaries of the RSE licensee;

- other related bodies corporate of the licensee (such as parent and sibling entities); and

- entities with certain control relationships with the licensee.

The concept of ‘entities with certain control relationships with the licensee’ can be understood through the definition of ‘connected entity’ as set out in the Superannuation Industry (Supervision) Act 1993 which includes an ‘associated entity’ under the Corporations Act 2001 and any prescribed entities. In contrast to an SRE for an Accountable Entity in the banking and insurance sectors, an SRE for an RSE licensee does not necessarily have to be a subsidiary of the licensee to have a material and substantial impact on it. Another point of difference for an SRE in the superannuation sector is that unlike other Accountable Entities, a related entity can be an SRE of more than one RSE licensee.

Accountable Persons

Individual accountability is created through the concept of Accountable Person.

An Accountable Person under the FAR is a person who:

- holds a position in an Accountable Entity or another entity being a parent entity (for non-RSE licensees) or an entity of which the RSE licensee is a connected entity (for RSE licensees); and

- because of that position, the person has senior executive responsibility for management or control of the accountable entity or of a significant or substantial part or aspect of the operations of the Accountable Entity or the Accountable Entity’s relevant group (comprising its SREs).

An Accountable Person also includes a person who:

- Has a prescribed responsibility or position –prescribed by way of Minister rules; or

- SRE – is a person holding a position in an SRE and because of that position has actual or effective management or control of the Accountable Entity, or a substantial part of the Accountable Entity’s operations or that of its relevant group.

Financial Accountability Regime Minister Rules 2022 (Exposure Draft), Accountable Persons – prescribed responsibilities and positions

On 12 September 2022, the government released an exposure draft and the explanatory statement for the Minister Rules for consultation which ended on 7 October 2022. These have not been updated at the time of writing.

The draft Minister Rules supports the FAR Bill 2022 and would prescribe:

- particular responsibilities and positions which cause a person to be subject to the FAR in the banking, insurance and superannuation sectors;

- the enhanced notification threshold, which is the total asset size above which an Accountable Entity is required to comply with additional notification obligations;

- the way that a written record can be authenticated in a proceeding as prima facie evidence of the statement it records; and

- the start of a financial year for an Accountable Entity for the purpose of working out the total asset size.

The draft Minister Rules sets out 13 responsibilities that cover senior executives with responsibility for management (and in some cases control) of specified activities and functions and clarifies that the prescribed responsibilities are distinct from the responsibility (typically lower level) of carrying out or executing the activity or function. It also prescribes the position of a member of the Accountable Entity’s board of directors (or equivalent), which means that each member of the Accountable Entity’s board of directors would be an accountable person under the FAR. Such a person is likely to have oversight of the Accountable Entity’s activities and functions and is therefore appropriate to be an Accountable Person.

Note: The Policy Proposal Paper released in July 2021 included senior executive responsibility for management of the Accountable Entity’s end-to-end product responsibility in the list of prescribed responsibilities. The draft Minister Rules released in 2022 no longer include this responsibility.

How will the FAR operate?

Four core sets of obligations

Similar to the BEAR, the FAR imposes four core sets of obligations:

- accountability obligations;

- key personnel obligations;

- deferred remuneration obligations; and

- notifications obligations.

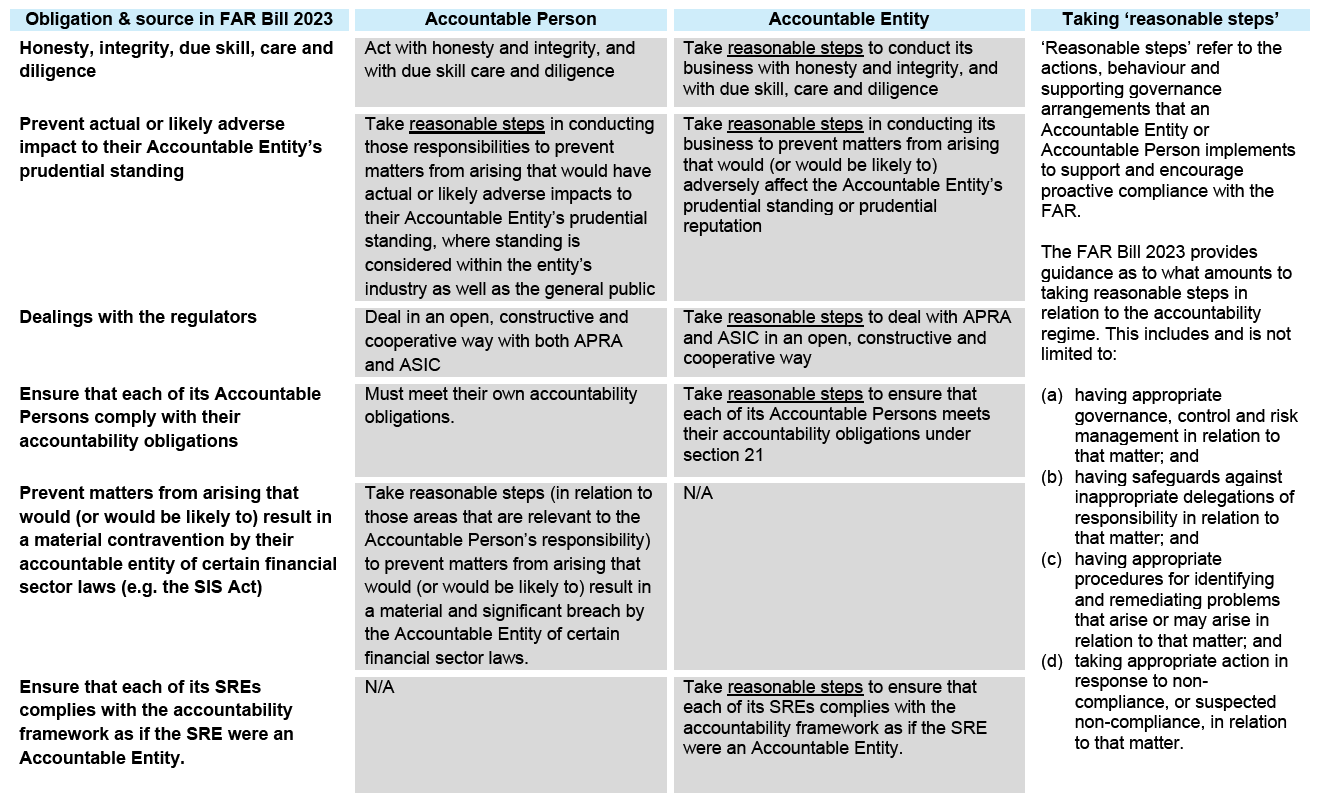

1. Accountability Obligations – Accountable Persons and Accountable Entities

The FAR imposes accountability obligations on both Accountable Persons and Accountable Entities – in relation to both conduct and prudential matters.

2. Key personnel obligations – Accountable Entities

The key personnel obligations apply to an Accountable Entity. Foreign accountable entities in the banking and insurance industries are only required to comply with the key personnel obligations in relation to the operations of their Australian branches.

The key personnel obligations are that an Accountable Entity must:

- ensure that the responsibilities of relevant Accountable Persons collectively cover all parts or aspects of its business, including the business of its relevant group (this obligation includes having Accountable Persons who are responsible for each of the responsibilities and positions prescribed in the rules made by the Minister);

- ensure compliance with any directions given by the regulator and take steps to ensure that its SREs do the same; and

- ensure that each of its Accountable Persons and those of its SREs have not been disqualified from being accountable persons by the regulator.

The Accountable Entity must also ensure compliance with the prescribed timings for the purpose of these obligations. It must make sure that each of its Accountable Persons and those of its SREs are registered with the regulator before that person starts the role as an accountable person. There are 3 exceptions to this requirement:

- Accountable Persons filling temporary vacancies or unforeseen vacancies have up to 90 days after becoming an Accountable Person to be registered;

- An Accountable Person who is appointed as director of an Accountable Entity at a general meeting has up to 30 days to be registered; and

- An entity that becomes an Accountability Entity after the application of the FAR to the industry the entity is licensed for will have 30 days, from the day the entity becomes an Accountable Entity, to register their Accountable Persons.

3. Deferred remuneration obligations – Accountable Entities

The deferred remuneration obligations generally apply to variable remuneration paid by the Accountable Entity (including other entities in the corporate group to which the Accountable Entity belongs) – i.e. remuneration which is conditional on an Accountable Person’s performance. The form of this variable remuneration could be cash, shares, options, and also other forms. The deferred remuneration obligations will apply in addition to APRA’s CPS 511 – Remuneration.

To comply with the deferred remuneration obligations under Part 5, the Accounting Entity must:

- defer payment of at least 40% of each Accountable Person’s variable remuneration for the relevant financial year for a minimum period of four years;

- have a remuneration policy that requires the variable remuneration of an Accountable Person to be proportionately reduced if they fail to comply with their accountability obligations;

- not pay the portion of variable remuneration that has been reduced in accordance with the remuneration policy; and

- take reasonable steps to ensure that their SREs comply with the above.

The deferred remuneration obligations do not apply if:

- the Accountable Person’s deferred remuneration in a particular financial year would be less than $50,000;

- the Accountable Person is filling a temporary or an unforeseen vacancy and hold the position for 90 days or less; or

- the Accountable Person’s total remuneration does not include any variable remuneration; or

- the variable remuneration relates to other work the Accountable Person performed outside their role as an Accountable Person.

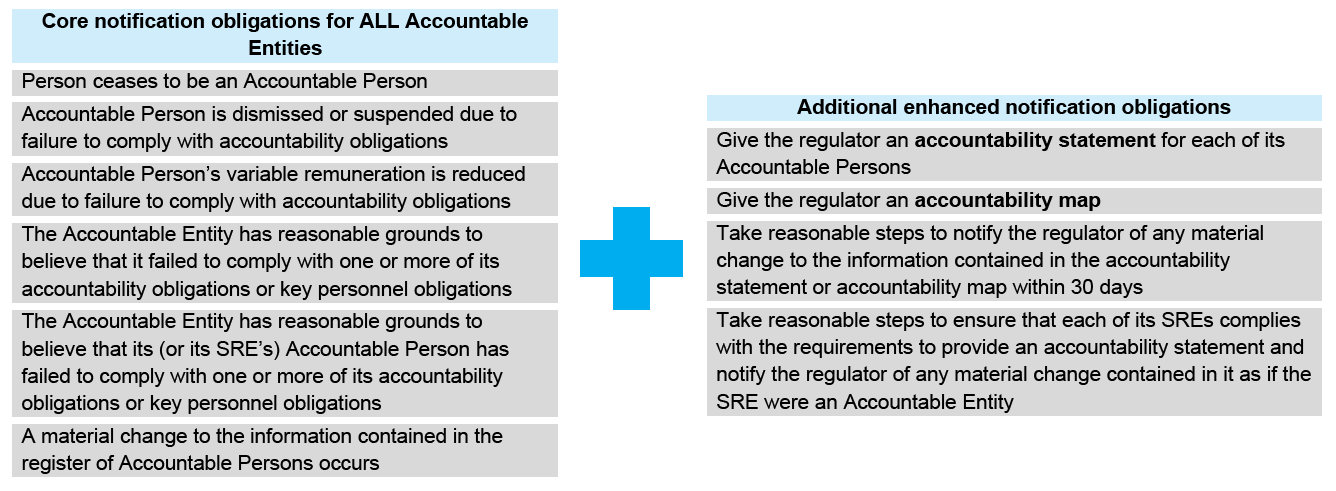

4. Notifications obligation – Accountable Entities

Under the FAR, an Accountable Entity must provide a regulator with certain information about the entity and its Accountable Persons. All Accountable Entities are required to comply with the core notification obligations, while a smaller group of entities are required to comply with the enhanced notification obligations.

These obligations are important to ensure the regulator has up to date information about the nature and influence of entities and persons who are subject to the FAR. The draft Minister’s Rules explains that the methodology is based on total assets reported to APRA in earlier financial years (broadly consistent with ADI methodology in BEAR). Consistency of approach across relevant financial sectors is intended to support understanding of, and compliance with the FAR.

An Accountable Entity meets the enhanced notification threshold at a particular time during a financial year of the accountable entity if, at the start of the financial year, its total asset size equals or exceeds the prescribed threshold. The total asset size is determined by the total assets value reported in a financial year, or the average total assets value across several final reports the Accountable Entity has submitted to APRA.

Enhanced notification threshold (in the 2022 draft Minister rules):

- ADIs: total assets size equals or exceeds $10 billion;

- General insurers: total assets size equals or exceeds $2 billion;

- Life companies: total assets size equals or exceeds $4 billion;

- Private health insurers: total assets size equals or exceeds $2 billion; and

- RSE licensees: total assets size equals or exceed s $10 billion.

Where one Accountable Entity (the first Accountable Entity) meets the enhanced notification threshold in a financial year of the entity, and it is related to another Accountable Entity (the second Accountable Entity), the second Accountable Entity also meets the enhanced notification threshold at that time. The draft Minister Rules clarifies that in working out the total asset size of an Accountable Entity, the start of the financial year may be before the Rules commence, or before the time when the entity starts being an Accountable Entity.

It is time to act now

The proposed changes have FAR-reaching consequences, so it is prudent to commence the implementation plan now if you have not done so already. We have extensive experience implementing the BEAR regime for banks/ADIs. Accordingly, we are well positioned to be able to assist you as FAR as you need.

Get the latest news insights and articles straight to your inbox, simply enter your details.

follow us