By Clement Ngai, Paralegal, and Benjamin Lyon, Paralegal

If your not-for-profit has been established as a company, the company directors have significant duties associated with their role in orchestrating the operations of the not-for-profit. Under the common law and the Corporations Act 2001 (the Act), obligations have arisen in order to protect members from improper behaviour by directors. However, this piecemeal development of the law has resulted in complex requirements and restrictions which are not always easy for directors to comprehensively understand. This is particularly so in the case of related party transactions which are instituted in Chapter 2E of the Act and are known to be legally complex and often confusing to understand.

In light of this, ASIC released Regulatory Guide 76 (RG76) in relation to “Related Party Transactions”, to assist public companies and their professional advisers in better governance and disclosure in relation to related party transactions. 1 Directors of not-for-profit companies should take particular caution in relation to potential related party transactions, not only to avoid the hefty penalties associated with breaches in this area, but also to ensure that transparency and accountability are a hallmark of their organisation.

Duties and obligations relevant to Related Party Transactions

Directors considering engaging in related party transactions must be aware that the provisions affecting directors entering related party transactions are not limited to the ‘Related Party Transactions’ chapter (Pt 2E) of the Act. Before specifically considering Part 2E of the Act and its provisions for related party transactions, directors should consider the following duties and obligations:

- Obligations concerning use of position and information: Under sections 182 and 183 of the Act, company directors have obligations not to use their position, or information acquired as a director, to gain an advantage for themselves or someone else, or cause detriment to the organisation.

- Obligation to give notice of material personal interest: Under section 191 of the Act, company directors have obligations to disclose to other directors any material personal interest. Furthermore, directors cannot vote on a matter in which they have a material personal interest, or attend directors’ meetings while the matter is being considered, unless ASIC or the other directors provide relief, in accordance with the requirements of the Act. Although this section does not apply to registered charities, similar obligations are imposed on charities through the ACNC regulations (Governance Standard 5).

- Fiduciary Duties: Under the law of equity, directors owe fiduciary duties towards their companies: a duty not to place themselves in positions of conflicting interests, and a duty not to make a profit at the expense of the company.

- Related Party Disclosures: Under the Australian Accounting Standards Board (AASB) related parties disclosure standards, AASB 124, not-for-profit public entities must make numerous disclosures about known financial relationships with related parties.

Related Party Transactions under Part 2E of the Act

What parties are covered under ‘related parties’ of a public company?

Section 228 of the Act contains a list of parties that are to be considered related parties of a public company. These include:

- controlling entities of the company;

- directors (of the company, or of any entity controlling the company);

- persons making up a controlling entity of a public company (where the entity is not a body corporate); and

- spouses, parents and children of the persons listed above.

It further includes:

- any entities controlled by the parties listed above;

- any entity that was a related party in the previous six months or (has reasonable grounds to believe that it) will be a related party in the future; and

- any entity that acts in concert with a related party on the understanding that the related party will receive a financial benefit if the company gives the entity a financial benefit.

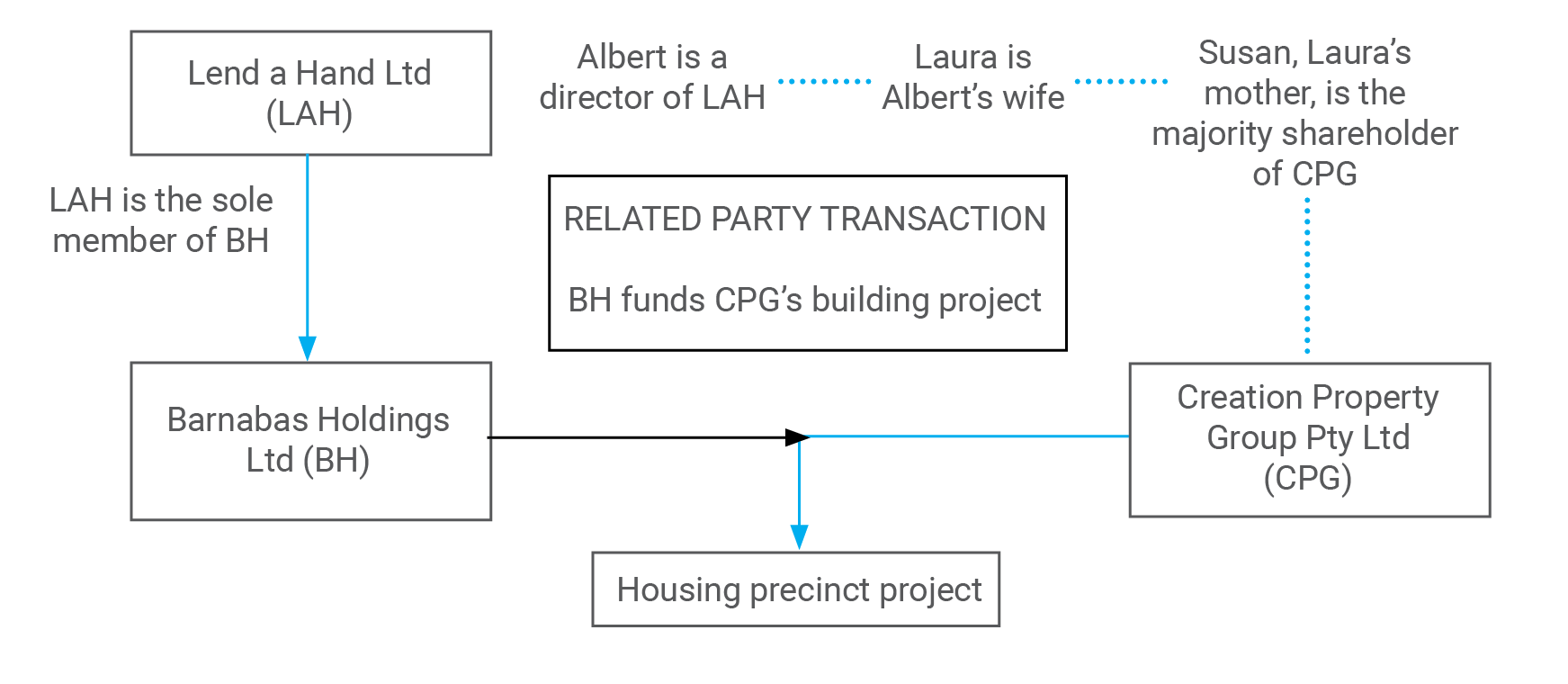

The following fictional example of a related party transaction demonstrates the wide potential scope of section 228: CPG is a related party of LAH, since it is controlled by the parent of a spouse of a director of LAH.

CPG is a related party of LAH, since it is controlled by the parent of a spouse of a director of LAH.

CPG is also a related party of BH, since LAH has control over BH and CPG is a related party of LAH, as explained above.

BH’s funding of CPG’s building project would therefore be a related party transaction under section 228 of the Act.

Why should our company be concerned?

In order to protect the interests of a public company’s members as a whole, section 208 of the Act requires the public company to obtain approval from its members when proposing to give a financial benefit to a related party. There are also exceptions to this requirement in sections 210 – 216 of the Act, as summarised below.

However, if a company fails to obtain member approval and none of these exceptions apply, a director involved may be liable to civil penalties. Furthermore, criminal penalties may even be relevant if the director’s involvement in the related party transaction is considered dishonest (s209(3)).

What significant exceptions are there to obtaining member approval?

The ‘arm’s length’ exception

A public company may provide financial benefits to related parties without member approval when the terms agreed would have been reasonable in the case that the parties were dealing at “arm’s length” (s210). RG76 describes an “arm’s length” relationship as “where neither bears the other any special duty or obligation, they are unrelated, uninfluenced and each acts in its own interests.” This is an objective test which considers several additional factors; however there is no established, step-by-step test. Due to this complexity, RG76 suggests that directors should only rely on this exception when they are ‘persuaded that the exception does apply, rather than it being merely arguable that it applies.’2

Reasonable remuneration for officers or employees

A public company may provide financial benefits to related parties without member approval, where the benefit is remuneration or a reimbursement of expenses incurred in the related party’s capacity as:

- an officer or employee of the company;

- an entity controlled by, or that controls, the company; or

- an entity that is controlled by the same entity as the company.The financial benefit must still be reasonable in the circumstances – e.g. reimbursements must correspond to invoices for the related party’s expenses (s211).

Payment to officers for indemnities, exemptions, insurance premiums and legal costs in respect of liabilities incurred as an officer

A public company may provide financial benefits to related parties without member approval where they are payments by way of indemnities, exemptions, insurance premiums, and legal costs if the payment is in respect of a liability incurred in the related party’s capacity as an officer of the company (s212). The benefit must be reasonable in the circumstances and the section must be read in light of restrictions on indemnities and insurance found elsewhere in the Act (ss199A-199C).

Benefits to or by a closely-held subsidiary

A public company may provide financial benefits to related parties without member approval, or receive benefits from them, where the related party is a wholly-owned subsidiary of the company (s 214).

Benefits that do not discriminate unfairly

A public company may provide financial benefits to a member of the company who is a related party without member approval, provided that the benefit is provided in the party’s capacity as a member and does not discriminate unfairly against any other members (s215).

Confidently avoiding liability

Member approval

Where there is still doubt in a director’s mind as to whether the statutory exceptions are applicable in the circumstances of a proposed related party transaction, it is advisable not to proceed without obtaining member approval. Material that will be put before members must be lodged with ASIC, in accordance with the process set out in the Act. Generally, this must be done at least 14 days before a notice convening the meeting is sent out to members. If the entities entering into related party arrangements wish to offer securities, disclosure documents will also need to be provided subject to the requirements of the Act and RG76.

Related Party Disclosure Policy

This is a recommendation that has been made by both the ACNC, and the Governance Institute of Australia. This could be in the form of a separate policy, within an existing conflict of interest policy, or within the board charter of the company. Furthermore, a company secretary should maintain and regularly update a register of directors’ material personal interests, and proposed related party transactions.

Expert Advice

Since breaches with regard to related party transactions are complex to determine and carry substantial penalties, this is an area of the law that requires particular care. If directors find that they do not have the knowledge or expertise necessary to assess all aspects of related party transactions, RG76 makes it clear that directors should obtain expert advice, 3 acknowledging that advice is not a replacement for the director’s careful consideration of the issue at hand. 4

Circumspection in relation to the applicability of exceptions, gaining member approval, and developing governance policies will work towards ensuring transparency, and accordingly building the public trust and confidence that is so crucial to achieving the goals of charities and not-for-profits.

1 Australian Securities and Investments Commission, Related Party Transactions, Regulatory Guide 76, 30 March 2011.

2 RG 76.94

3 RG 76.90

4 RG 76.91

Get the latest news insights and articles straight to your inbox, simply enter your details.

follow us